Every January, millions of Americans who rely on Social Security receive a familiar — and closely watched — annual payment adjustment. In 2026, this cost-of-living adjustment (COLA) is in focus again, offering a modest increase to benefits at a time when many retirees and disabled workers are feeling the squeeze from rising costs. (The Times of India)

What Is COLA and Why It Matters

The Cost-of-Living Adjustment (COLA) is an automatic annual increase in Social Security and Supplemental Security Income (SSI) benefits, designed to help recipients keep pace with inflation. Rather than being a true “stimulus” in the traditional government-policy sense, COLA functions as a built-in safeguard against rising prices — especially for basic living expenses. (Social Security)

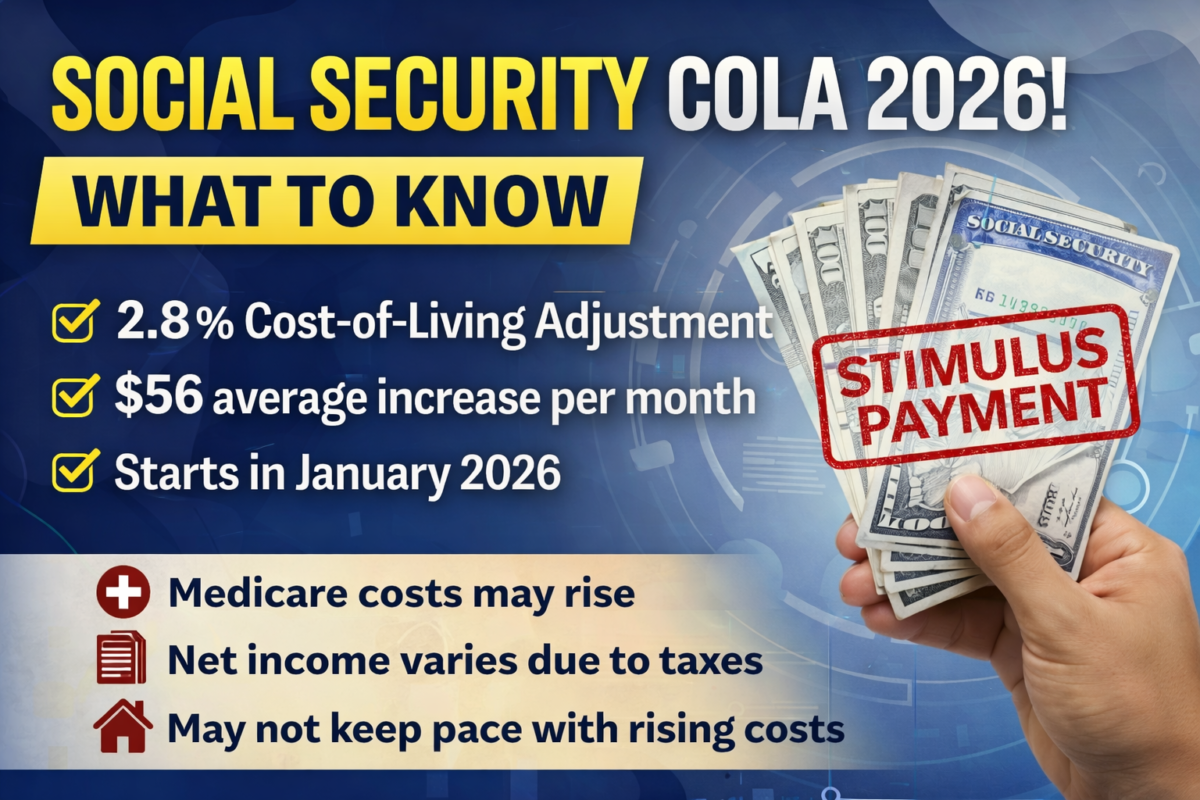

For 2026, the Social Security Administration (SSA) has announced a 2.8 % increase in benefits, compared with a 2.5 % rise in 2025. (Social Security)

How Much More Will Beneficiaries Receive?

A 2.8 % COLA means real money for beneficiaries:

- The average retired worker’s benefit will rise by roughly $56 per month starting in January 2026, bringing monthly payments to about $2,071 on average. (The Times of India)

- Married couples receiving dual benefits will see their combined totals rise proportionally higher. (The Times of India)

- SSI recipients — including low-income seniors and people with disabilities — also benefit, with individual maximums rising to higher thresholds. (The Times of India)

This increase is automatic: beneficiaries do not need to apply or re-register to receive it. (Social Security)

Why It Feels Smaller Than You Expect

Despite headlines calling it a “stimulus,” many recipients say the increase doesn’t stretch far enough. Here’s why:

- Healthcare Costs Eat Into the Raise – Medicare Part B premiums often rise at the same time as COLA, reducing the net benefit people actually take home. For many retirees, that Medicare increase can erase a sizable portion of the new boost. (The Times of India)

- Taxes and Deductions – Some retirees still pay federal income tax on part of their benefits if they have other income, further shrinking the effective increase. (The Times of India)

- Living Costs Still Outpacing COLA – While COLA tracks inflation, it’s based on a specific consumer price index that may not reflect real-world costs for seniors — particularly for healthcare, housing, and prescription drugs. Many beneficiaries report that the increase doesn’t fully cover their rising expenses. (The Economic Times)

When You’ll See the Money

Payments reflecting the 2026 COLA begin arriving in January:

- SSI recipients often see the raise as early as December 31, 2025. (Social Security)

- Social Security retirees and disability beneficiaries receive the updated benefit starting with the first checks of January 2026. The exact date depends on birth date and payment schedule. (The Times of India)

Who Benefits Most — and Why It Still Matters

COLA primarily benefits Americans who rely heavily on Social Security as a major part — or even the sole source — of income. That includes:

- Retirees

- People with disabilities

- Survivors and dependents

- Low-income seniors on SSI

For these groups, even a modest boost can make practical differences in covering food, utilities, rent, and medicines. Because the program affects nearly 75 million people nationwide, the fiscal impact is massive — around $1.6 trillion in annual payouts. (The Times of India)

Even though it’s not technically a “stimulus,” the COLA functions similarly: it injects billions into household budgets at the start of the year, providing predictable support for essential expenses.

Final Takeaway

The 2026 Social Security COLA may not feel like a windfall, but it plays a crucial role in helping millions of Americans keep pace with inflation. While healthcare costs and taxes blunt some of its impact, the automatic benefit increase remains a key part of financial stability for retirees and vulnerable populations.

Longer-term financial planning — including savings and diversified income strategies — remains vital alongside Social Security benefits, especially as living costs continue rising.